How to Turn Paper Gains into Real Returns before Your Portfolio Company Exists

A plain-language guide to using SPV structure and secondary sales to deliver liquidity to LPs on your timeline, not the market’s.

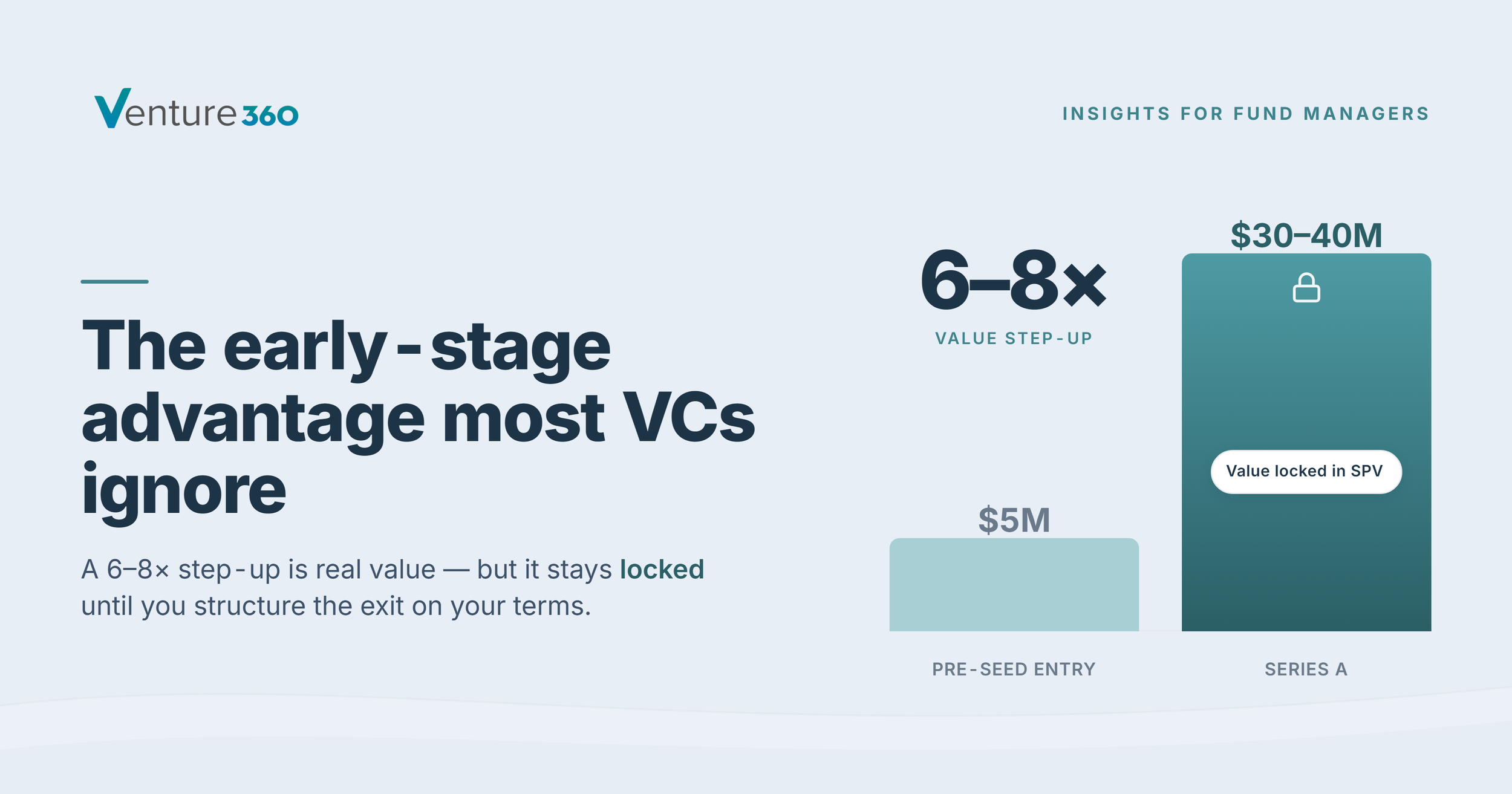

The early-stage advantage most VCs ignore

When you invest at a $5M valuation and the company raises a Series A at $30-40M, your position is now worth six to eight times what you paid. That's real value - but it's trapped. The company hasn't exited. No acquisition, no IPO. Just a number on a spreadsheet.

This is the moment most managers wait out. But there's a smarter move available to you, and it starts with how you structured the investment in the first place.

Your edge as an early-stage manager: larger funds can't deploy meaningfully at $5M valuations. You can. That asymmetry is only useful if you've built the structure to act on it.

Why traditional venture keeps LPs waiting

In conventional venture, the timeline runs like this: you invest, help the company grow, then wait for an acquisition or IPO - sometimes a decade later - before distributing anything to your LPs. For emerging managers, that's a real problem.

LPs with shorter time horizons get impatient. Your fund metrics look muted while you're holding paper gains. And it's hard to show a track record to investors in your next fund when nothing has actually been realized.

The key question: What if you could show realized returns - not just paper gains - while your portfolio company is still growing?

The SPV structure: how it changes what's possible

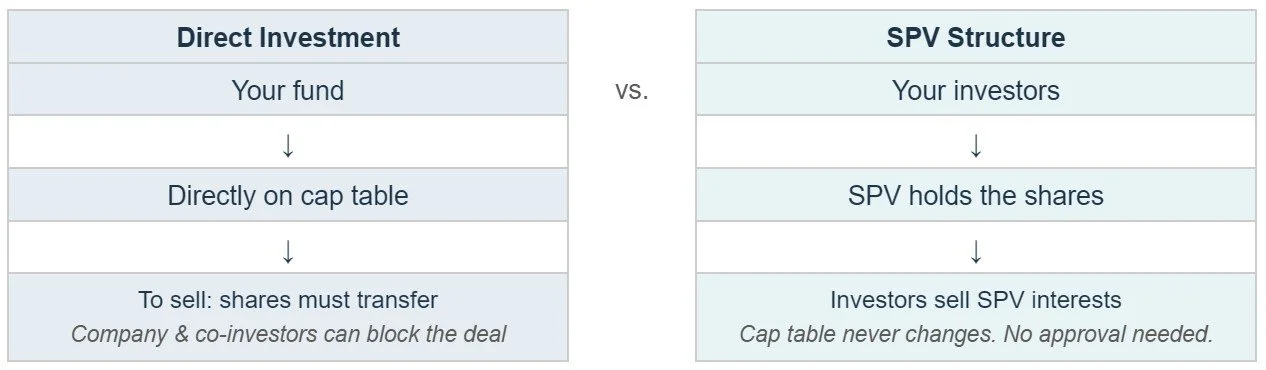

Most early-stage investments are made directly onto a portfolio company's cap table. Selling that position on the secondary market is slow and complicated - the company and other investors often have rights (called ROFR, or right of first refusal) that let them block or match any transfer.

Investing through a single-asset SPV changes the equation entirely.

When an investor in your SPV wants to sell, they're selling their interest in the SPV - not the underlying shares. The company's cap table never changes. Right of first refusal provisions don't apply, because no shares are transferring hands.

The result: a secondary transaction you can execute on your timeline, right after a Series A has validated the company's trajectory and reset market perception of its value. One investor can take early liquidity while others stay in. Everyone wins.

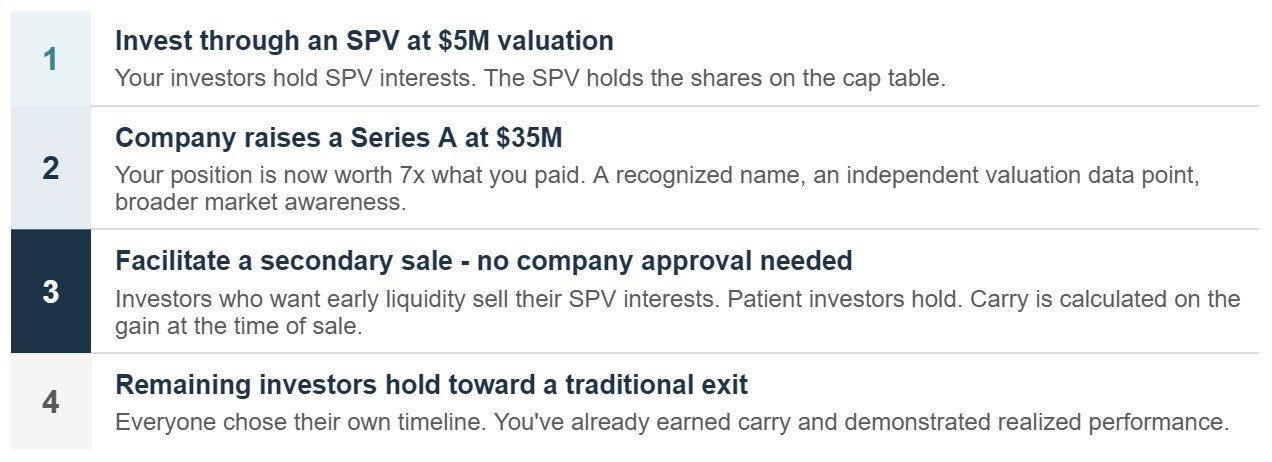

What this looks like in practice

The carry structure that makes this work for you

This isn't just good for your LPs. When carry is structured on an investor-by-investor basis - rather than at the aggregate fund level - every secondary sale that closes at a gain triggers carry at that moment, not years down the road when the fund winds down.

That's a meaningful difference: earlier cash flow to you as a manager, and a clear performance story you can show to current and future LPs while the fund is still active.

You're not just facilitating liquidity - you're effectively running a mini marketplace inside your investor network. You bought early at a low valuation. The Series A gave you a recognized name and a market price. New investors who missed the early round may now want in. The SPV structure makes clean transfers possible.

Expanding beyond your existing network

Your LP network has limits. When you're sourcing buyers for SPV interests, the right buyer may not already be in your circle. They might have learned about the company through other channels and been looking for a way in.

Broker-dealer relationships solve this. Rather than being constrained to your existing network, a broker-dealer can introduce SPV interests to a much broader universe of accredited investors and institutional buyers - without requiring you to publicize your deals or compromise confidentiality.

You control the process. The broker-dealer expands who can participate. The result is a more liquid, more competitive market for your SPV interests - which benefits both sellers seeking fair value and buyers seeking access.

Building this into your process from the start

This approach works best when it's built in from day one - not retrofitted. That means investing through single-asset SPVs, structuring carry to reflect individual-level economics, and working with an administrator that can scale secondary trading, not just close one deal.

Your edge as an early-stage manager isn't only about getting into the right deals. It's about capturing that value on your terms, not the exit market's. Venture360's SPVs are structured around these principles, and our affiliated broker-dealer helps you position for secondary trading at scale.

This material is provided by Venture360 for informational and educational purposes only and is intended for venture capital and investment managers.

The structures, strategies, and examples described herein are illustrative and are not intended as legal advice. The use of special purpose vehicles (SPVs), secondary transactions, and related structuring considerations are subject to applicable securities laws, contractual restrictions (including transfer limitations), and market conditions, and may not be appropriate in all circumstances. There can be no assurance that any strategy described will achieve its intended outcome or result in liquidity.

Venture360 provides administrative and operational support services, including SPV formation and fund administration. Any secondary transaction facilitation may involve an affiliated broker-dealer and will be conducted in accordance with applicable regulatory requirements.